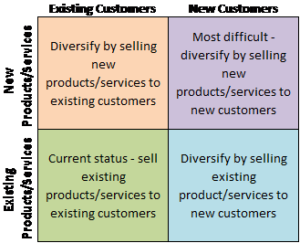

We’ve all heard the adage, “Don’t put all your eggs in one basket.” How does this advice hold up for nonprofit income? Before we continue our Nonprofit Chart of Accounts Grand Tour into income accounts (here’s the guide to the Tour of balance sheet accounts), first let’s consider the concept of income diversification. Income accounts…

Read More

Over $1.85 trillion dollars of income was reported by public charities filing Form 990 or 990-EZ, based on 2016 IRS data compiled by The Urban Institute, National Center for Charitable Statistics. Where does all that money come from? Specifically we are focusing on income of 501(c)(3) public charities. For comparison’s sake, here are common types…

Read MoreDo you know the biggest secret to keeping good books? Well, we’re going to let you in on it. It’s managing the balance sheet. Many of the problems we’ve seen with bookkeeping can be traced back to not keeping an accurate balance sheet. We see many people focus only on the profit and loss report, and…

Read MoreOver $50,000 gone was the latest estimate. Sadly this is a true story. The administrative assistant, a trusted employee, had been using her organization credit card to pay for personal expenses. She carried out the fraud over about a year, though no one will probably ever know exactly when the thefts started or exactly how…

Read MoreWe keep getting “the question.” Hint — it’s not “Would you be our treasurer?” Though we get that one a lot, too. No, the question we refer to is when our client points to the net assets section of the organization’s balance sheet and asks, “Is that the money we have to spend?” It’s a…

Read More

“Today, there are three kinds of people: the have’s, the have-not’s, and the have-not-paid-for-what-they-have’s.” ~Earl Wilson When it comes to nonprofit organizations, nearly all fall into the “have-not-paid-for-what-they-have’s” category, even if managers are scrupulous about paying everything on time. That’s because at any given point in time, a nonprofit organization with active operations in pursuit…

Read MoreWhen we talk to nonprofit organization leaders about budgeting, we find they are usually thinking in terms of budgeting cash in and cash out. Even if you budget on cash basis (as opposed to accrual basis), you still need to capitalize and depreciate fixed assets. Accounting for fixed assets throws a big monkey wrench into…

Read MoreSo you bought a laptop computer. That’s great! Quick question: Is it an asset or is it an expense? Answer: It depends. Don’t you hate that? For one organization the laptop is an asset. For another organization, it’s an expense. It all depends on the organization’s capitalization threshold. The what? Capitalization Threshold Let’s define capitalization…

Read More

Aging. Now there’s a topic we can all relate to! But I’m not talking about the kind of aging you and I experience each day. I’m talking about accounts receivable aging. The biggest difference is that accounts receivable, unlike you and me, do not get better with age. In our last post, Why Care About…

Read More

“We have pledges receivable, but they are not on our books. Shouldn’t they be in our books?” Such began our consulting engagement with a local nonprofit organization, Spring Center (not the real name). Pledges Receivable and Accounts Receivable Our Chart of Accounts Grand Tour continues with the next type of account commonly found on the…

Read More